In August 2025, the Supreme Court delivered a sharp and long-overdue intervention in India’s power distribution sector. It directed all states (Commissions) to ensure that electricity tariffs are cost-reflective and that any existing regulatory assets be liquidated within a maximum of seven years, with a clear trajectory and roadmap for their liquidation.The Court also tasked the Appellate Tribunal for Electricity (APTEL) with monitoring the implementation of these directions. Delving deeper into the causes of delays in tariff revisions and the continued build-up of regulatory assets, the Court explicitly questioned the functioning of the State Electricity Regulatory Commissions (Commissions). It observed that, despite their functional autonomy under the Electricity Act, 2003, the decisions of the Commissions do not inspire confidence and emphasised that they must guard themselves against “regulatory failure,” particularly “regulatory capture.”(1)

Nearly eight months after the Supreme Court issued clear directions, a review of actions taken by most Discoms do not offer much assurance in the timely liquidation of regulatory assets (RA). Most have responded with little more than formal submissions and unspecific timelines, as discussed further, and concrete action has been limited. Rajasthan stands out as a rare case where the directive has translated into measurable progress, with a 38 per cent reduction from the FY 2023 baseline.(2)

What leads to regulatory assets?

Regulatory assets (RA) are financial tools used by Discoms to manage the gap between the costs incurred in supplying electricity and the revenues generated. When Discoms are unable to recover certain costs immediately, regulatory assets allow them to defer those costs to future periods. While the practice may be useful in providing temporary relief to utilities facing short-term cash flow challenges, its continued use to avoid tariff revisions leads to accumulation, which has significant long-term implications for the financial health and sustainability of Discoms. At the national level, ICRA (Investment Information and Credit Rating Agency of India Limited) estimates regulatory assets of major state Discoms at approximately Rs. 3 trillion, with Tamil Nadu, Uttar Pradesh, Maharashtra, Delhi and Rajasthan accounting for a substantial share.(3)

The legal architecture under the Electricity Act has always mandated that tariffs should reflect actual costs. Multiple Government of India reform schemes and policy frameworks have consistently emphasised cost-reflective tariffs and timely revisions. Yet, implementation has faltered due to multiple factors, including political sensitivities around electricity pricing, affordability concerns, delayed filings by Discoms, and inadequate action by them to address these issues. Despite their role as custodians of tariff determination in the sector, the Commissions often fail to ensure timely tariff revisions due to ‘regulatory capture’, that is, a lack of functional autonomy, as noted by the Supreme Court (4). It has to be noted that regulatory assets, though widely used, remain loosely defined in statutory practice, as they are neither a statutory concept nor explicitly provided under the Electricity Act. Different Commissions have variously referred to them as Deferred Revenue Gap, Revenue Gap, Unfunded Revenue Gap, or Deferred Cost Recovery.

What has been done by the States on the directives?

Among Indian states, Tamil Nadu, Delhi, Rajasthan, and Maharashtra account for a significant share of regulatory assets in the country. In response to the Supreme Court’s directions, their respective Commissions have submitted varied replies to the Suo-moto petition initiated by APTEL in August 2025 to monitor compliance as of date.

The Tamil Nadu Commission (TNERC) initially submitted that since the state government would take over the entirety of the regulatory assets, it need not comply with the directions, including auditing its Discoms. (5) When APTEL disagreed (6), TNERC filed a writ before the Supreme Court challenging both the APTEL proceedings and the relevant Rule under the Electricity Amendment Rules, 2024, which formed the basis of the Court’s August 2025 judgment. At the same time, TNERC submitted in April 2026 (7) that it would furnish the final audit report by the end of April and issue tariff orders, including carrying costs, in June (8).

On the other hand, Maharashtra initially denied the existence of any regulatory assets in its submissions. Following APTEL’s intervention, it subsequently acknowledged the quantum of RA and issued its ARR (Annual Revenue Requirement) order outlining a prospective plan for their liquidation, including carrying costs (9). However, the Commission has sought additional time until May 2026 to submit the requisite audit report (10). Delhi, with regulatory assets of Rs. 38,552 crores sought an extension until July 2026 to even commence the liquidation process. APTEL rejected this plea in its order dated April 20, 2026, noting that the Commission’s repeated delays, despite undertakings to the Supreme Court, the Delhi High Court, and APTEL, rendered its conduct “malafide.” Delhi Commission was directed to commence liquidation within three weeks (11).

Nearly a year after the Supreme Court’s directive, lot of states remain confined to procedural compliance, repeated extensions, and ongoing audit processes. Rajasthan, by contrast, has demonstrated tangible action, with significant surcharge collections and a clearly defined recovery target.

Rajasthan’s approach towards RA liquidation

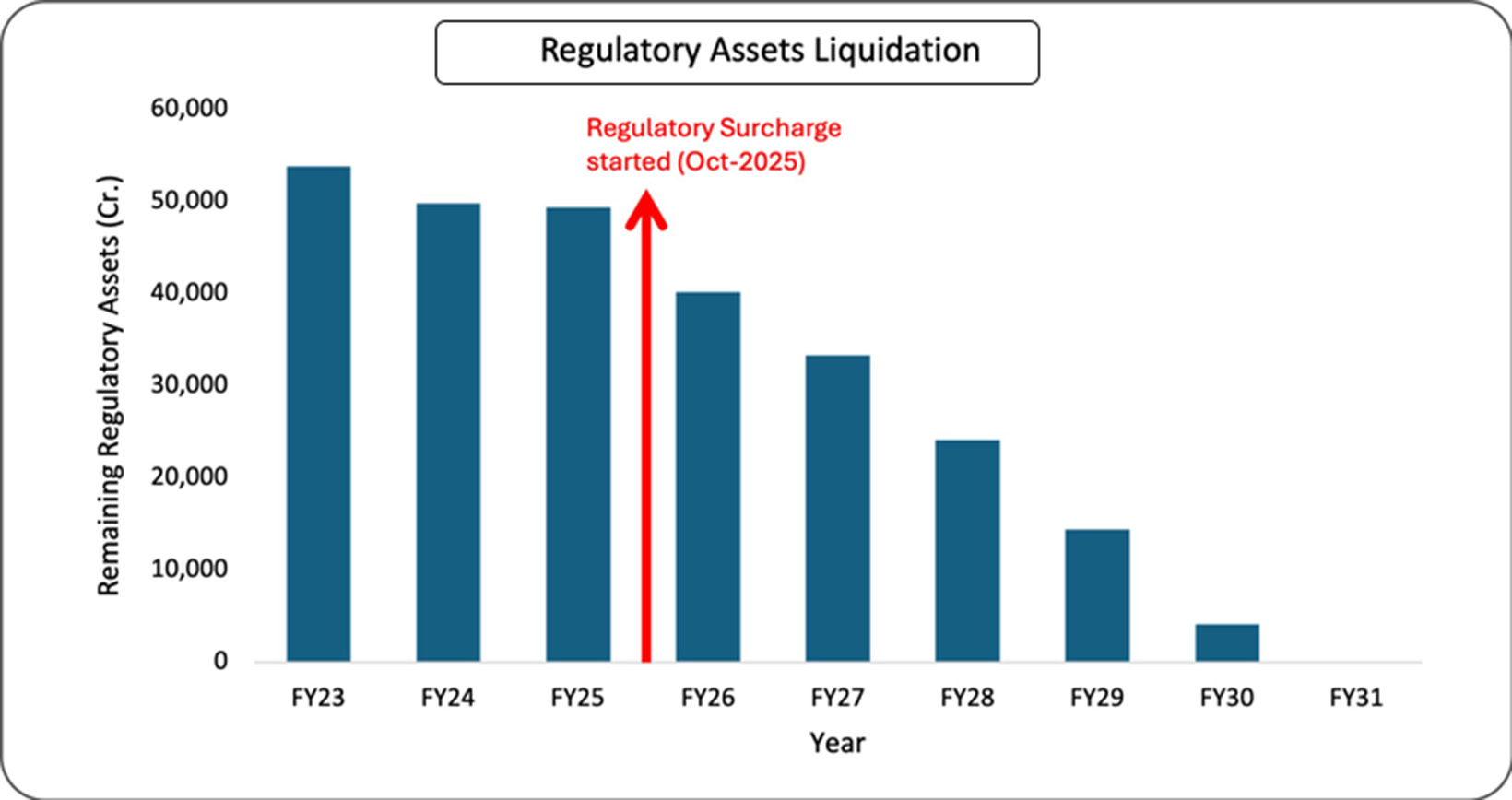

Diverging from this trend, Rajasthan’s approach underscores both the feasibility of action and the presence of political and regulatory will. The state’s accumulated regulatory assets had reached approximately Rs. 53,824 crores by FY 2022–23.

The turning point came in October 2025, when the Rajasthan Commission introduced a dedicated Regulatory Surcharge in its Tariff Order based on Discom submissions in their petitions. The surcharge design was attempted to be equitable, set at Rs. 0.42 per unit for domestic consumers with consumption below 100 units per month and Rs. 0.72 per unit for all other consumer categories, over and above the approved tariff. Thereafter, in the last six months of FY 2025–26, alone the three Discoms in Rajasthan (Jaipur, Ajmer and Jodhpur Discom) together collected Rs. 3,341 crores for the recovery of RA. The Commission, while approving the tariff for FY 2026–27 in March 2026, confirmed the continuation of the surcharge at Rs. 0.56 per unit for domestic consumers using up to 100 units and Rs. 0.86 per unit for all other categories, to be levied over and above the base tariff. For FY 2026–27, the Commission has set a target of Rs. 8,663 crores across the three Discoms. By the end of FY27, the outstanding balance is projected to decline to Rs. 33,298 crores, a 38 per cent reduction from the FY 2023 peak. The Commission’s proactive approach of ensuring separate accounting of the surcharge specifically for the liquidation of regulatory assets, rather than using it for cost-revenue gap management, also ensures this decline.

If we assume the current trajectory of demand growth, a constant interest rate of 10.5 per cent, and a continued surcharge levy by Discoms, the entire regulatory asset pool could be liquidated by FY 2030–31. (Refer to Figure 1)

The silent burden of carrying costs

The interest burden on deferred regulatory assets, or carrying costs, is usually transferred to consumers via tariffs. As this interest continues to accrue until recovery, it significantly increases the overall burden beyond the original liability. In the case of Rajasthan, the reduction in the principal amount of RA also leads to a decline in carrying costs. In FY 2024, the carrying cost burden translated to Rs. 0.68 per unit of consumer tariffs, which is projected to fall to Rs. 0.22 by FY 2029 and to a near negligible Rs. 0.03 by FY 2031. Consumers are likely to receive tangible relief in base tariffs well before the surcharge is fully phased out. (Refer to Figure 2)

.jpg)

The road ahead

In the case of Rajasthan, the State Commission adopted a more assertive approach by approving a structured mechanism to liquidate RA. This was supported by cost optimisation by State Discoms, especially in power procurement, alongside political willingness to pass through all costs, including regulatory surcharges, despite the sensitivity of such increases. The experience highlights the value of dedicated, ring-fenced mechanisms designed with equitable coverage across consumer categories, supported by clear annual targets and a time-bound implementation roadmap. Equally, sustained tariff discipline can prevent fresh accumulation of RA. Such measures can help States move beyond procedural submissions and instead drive tangible progress.

One critical issue that needs addressing is how regulatory assets are accounted under varied heads and their treatment within the ARR process, which leads to discrepancies in the estimation of actual amounts. The States also propose varied approaches to resolving these regulatory assets, which require closer scrutiny and monitoring. The role of Commissions in this context can be pivotal and will require them to exercise the functional autonomy granted under the legal framework governing the sector. Notwithstanding, the core issue is not the absence of regulatory tools or legal backing, but rather the lack of political will and institutional discipline.

It is important to note that even in Rajasthan’s case, the liquidation of regulatory assets addresses only part of the issue. The Rajasthan Commission’s Tariff Order for FY27 itself highlights deeper challenges in Discom operations, including a high prevalence of defective meters, inefficient power procurement practices, weak planning and demand forecasting, slow progress in reforms and scheme implementation, and concerns around data reporting. Many of these issues stem from structural factors such as Discoms serving as the end point for risks across the power sector value chain, complicated by limited autonomy, governance challenges, and broader political economy dynamics. Without addressing these structural weaknesses, there is a risk that new regulatory assets will continue to accumulate even as existing ones are cleared. For regulatory asset liquidation to serve as a catalyst for long-term sectoral sustainability, these underlying structural challenges must be recognised upfront, prior to any policy or reform action targeting Discoms.

The article is authored by Siddhant Singh, Research Associate at CEEP and Anshuman Gothwal, Co-founder and Director-Programs at CEEP.

References

1. BSES Rajdhani Power Ltd. & Ors. v Union of India and Ors., 2025 INSC 937.

2. Authors’ analysis.

3. ICRA Limited. (2025). Significant tariff hikes required to liquidate discoms’ regulatory assets in line with apex court directive.

4. BSES Rajdhani Power Ltd. & Ors. v Union of India and Ors., 2025 INSC 937.

5. APTEL. (2025, Sept. 26). OP No. 01 of 2025.; and APTEL. (2025, Oct. 30). OP No. 01 of 2025.

6. APTEL. (2025, Dec. 02). OP No. 01 of 2025.

7. APTEL. (2025, April 02). OP No. 01 of 2025.

8. APTEL. (2025, April 15). OP No. 01 of 2025.

9. APTEL. (2025, Sept. 26). OP No. 01 of 2025.

10. APTEL. (2025, April 15). OP No. 01 of 2025.

11. APTEL. (2025, April 20). OP No. 01 of 2025.

Please ensure all required fields (*) are filled out accurately.